Hi Everyone,

This year SPACs have been the center of attention in the public markets. So far there have been 151 U.S. IPOs consisting of 61 SPAC IPOs. A renewed evolution of companies skipping the traditional IPO process and partnering with high profile investors or entities is transforming rapidly. Today we will breakdown SPACs, special purpose acquisition companies with the goal aimed to capture the greatest wealth opportunities in the market.

Business Summary:

A SPAC (Special Purpose Acquisition Company) is a “corporate shell” company, also more commonly known as a blank check company, sponsored by an experienced investor, or investing entity. The SPAC company goes public by issuing shares to raise money from investors with the plan to acquire or merge with a private company. The merger or acquisition allows the private company to go public without going through the traditional IPO process.

Originally SPACs have been around since the late 1980s focusing on small-cap companies that could not go public through the traditional process. Initially, this attracted penny-stock promoters creating fraudulent activities. But since then with regulation, SPACs have experienced an evolution and gained a lot of coverage with influential investors such as Chamath Palihapitiya, regarding Virgin Galactic and Opendoor, and Bill Ackman’s recent $4 billion behemoth raise.

For investors, SPACs offer a low-risk entry to a large public offering and the target company goes public relatively quickly avoiding the IPO window and preserving the management team.

Market Landscape:

The number of public companies in the U.S. has been on a steady decline. In 1996 sources have highlighted that there were around ~7,300 domestic companies listed on the U.S. stock exchange. Today that number is hovering around ~4,000 representing a ~45% drop. As of 2020 YTD, we have had 151 companies enter the public market. The traditional IPO process can be an expensive drawn-out process consumed with high fees before shares are sold. With private capital readily available through a robust VC industry, companies are holding off longer to access the public market. As a result, it is important to note that companies have increased in size through years of acquisitions and business maturity. With companies that are larger in value and revenue, the high potential returns are usually reaped by the private investors that are taking on the risk. More recently, SPACs have re-emerged in the spotlight as an opportunity to take private companies public at an earlier stage without the overdrawn process of an IPO. This trend reveals that public investors need to have the opportunity to participate earlier in the growth stage of the company to have access to higher potential returns. Of course, with high potential returns comes high risk as well.

SPAC Landscape:

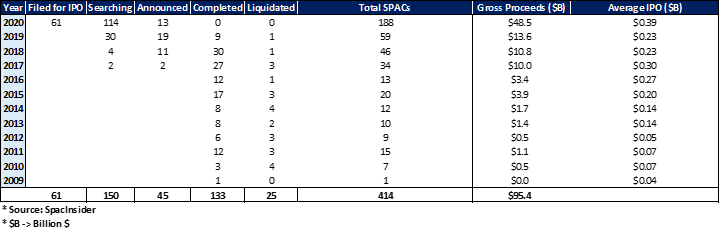

This year SPACs have stolen the spotlight. According to Pitchbook Data, as of May, SPACs represented 38% of IPO filings. In 2019, there were 59 SPAC IPOs amounting to $13.6 billion, and in 2020 127 SPAC IPOs amounting to $48.5 billion. This is an increase of 256% YoY.

Advantages:

For investors and the target companies there are advantages when it comes to the SPAC process:

Quick to Market: SPACs typically take three to four months to clear registration with the SEC, which tends to be shorter than the average length of time it takes to during the traditional IPO process that can range between six to nine months

Liquidity: Shareholders of acquisition targets can achieve instant liquidity by merging with a SPAC because they become shareholders of a public company

One Targeted Deal: The SPAC is limited to one acquisition deal. But after they complete that acquisition, they can act, acquire, or operate as any other public company

SPAC Sponsor: The success of the SPAC also relies on the reputation and brand of the sponsored investor. A strong reputable sponsor will create a lot of confidence to investors willing to participate. Usually, the investor is very experienced with a strong track record. The target company will benefit from a knowledgeable member of the SPAC team

Time Limitations: There is a time limit that forces the SPAC team to find a target (18-24 months). This gives investors assurance that a deal will be finalized in a specific time

Disadvantages:

Due Diligence: There is less scrutiny in the process involving a SPAC compared to a traditional IPO Process. This usually depends on how effective a SPAC sponsor is in their respective fields: (Example: Nikola)

Dilution: SPACs provide investors warrants, which means if the stock increases in price then the target company must provide more shares to the SPAC investor resulting in a dilution for the target companies’ original shareholders

SEC Regulation: Once the target company merges with the SPAC company, they are liable to satisfy SEC requirements immediately. The one-year grace period usually afforded to companies during a traditional IPO process does not apply to SPACs

Investment Banking Fees: Banks rack in fees (~10%) for their role in structuring the SPAC pre/IPO and during the merger/acquisition process. While the overall costs of an IPO are still higher during a traditional process, fees are still high for underwriters in the process compared to a direct listing process.

Target Company: Investors do not have an idea of what private company is being targeted in a SPAC IPO. As a result, the opportunity cost of investing in an asset that provides a vague direction of the potential private company to be acquired is present. Investors can certainly pull out before the merger if they don’t like the target company but would have missed additional opportunities during that time frame.

SPACs Structure:

SPAC will undergo the typical IPO process to file with the SEC and then begin raising the funds.

Founders invest initial capital to form the SPAC

Sponsor will purchase founders shares to ensure that they maintain 20% of the equity post-IPO

Bill Ackman made a change to his SPAC removing founders share and creating a similar private equity structure with carried interest and hitting a hurdle rate of return

IPO is made of units which are common shares and warrants

Public investors purchase units, which are made up of one share of common stock and a fraction of a warrant to purchase common stock in the future. The price is usually $10.00 per unit.

Only whole warrants are exercisable at $11.50 per share. They become exercisable 12 months after the SPAC IPO

IPO proceeds and initial capital contributed to the SPAC are placed in a trust account until the acquisition or merger occurs

The sponsor of the SPAC will also seek additional investment vehicle known as a PIPE (private investment in public equity) to fund the acquisition of the merger of the company. The investors experience lower fees for the opportunity to participate in the process

SPACs are also subject to time restrictions for the target company and operations.

The company must buy a business in less than 24 months

Market value of the business must be 80% or more of the SPACs trust assets

A couple of key notable SPAC transactions are:

Pershing Square Tontine Holdings: (PSTH)

Price: $22

$4 billion capital raised

Churchill Capital Corp. III: (CCXX)

Price: $10.29

$1.1 billion capital raised

Social Capital Hedosophia Holdings Corp. II: (IPOB)

Price: $12.39

Current Funds in Trust: $414 million

-Igli

You can access and download the detailed report here which will include our ~1,500 words summary. If you like the content please make sure to share this newsletter, share this post, or subscribe (if you have not already)!